Table Of Content

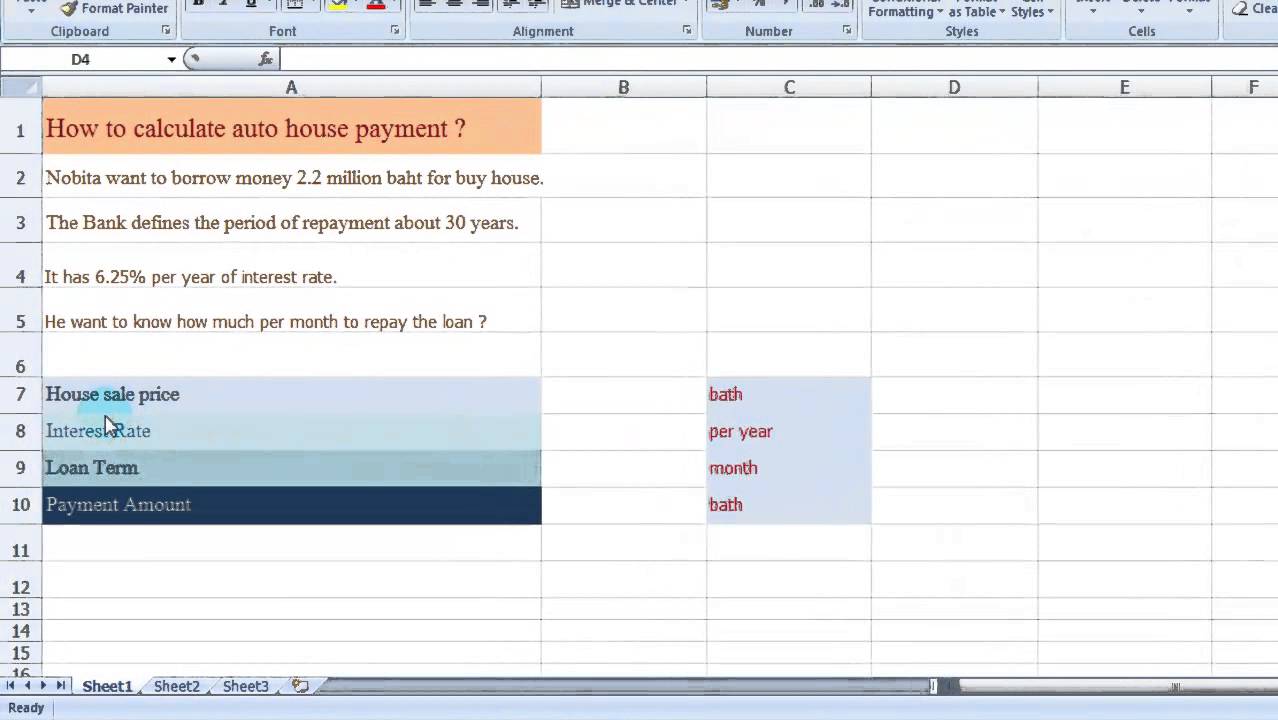

Most lenders allow you to include your property insurance in your monthly mortgage payment. Just like with PMI, the monthly amount is put into an escrow account, and the bill is paid on your behalf. The most significant factor affecting your monthly mortgage payment is the interest rate. If you buy a home with a loan for $200,000 at 4.33 percent your monthly payment on a 30-year loan would be $993.27, and you would pay $157,576.91 in interest.

HOA Fees

Apart from government-sponsored loans, borrowers also have the option to take jumbo mortgages. This is useful if you need particularly large financing to purchase expensive property. As previously mentioned, jumbo mortgages are non-conforming loans that exceed the federal loan limits prescribed by the FHFA. These are offered by private lenders such as banks, non-bank mortgage companies, and credit unions. Estimated monthly payment and APR calculation are based on a down payment of 25% and borrower-paid finance charges of 0.862% of the base loan amount.

Start your home buying research with a mortgage calculator

The homeowners insurance premium is the yearly amount you pay for the insurance. Many home buyers pay for this as part of their monthly mortgage payment. The “taxes” portion of your mortgage payment refers to your property taxes.

Veteran Home Loan Center

Short-term mortgages offer less protection against changing interest rates because you need to renew them more frequently. Mortgage refinance is the process of replacing your current mortgage with a new loan. Often people do this to get better borrowing terms like lower interest rates. Refinancing requires a new loan application with your existing lender or a new one.

If you don’t consider them all, you may budget for one payment, only to find out that it’s much larger than you expected. Basic amortization schedules do not account for extra payments, but this doesn't mean that borrowers can't pay extra towards their loans. Generally, amortization schedules only work for fixed-rate loans and not adjustable-rate mortgages, variable rate loans, or lines of credit. Getting a mortgage should always depend on your financial situation and long-term goals. The most important thing is to make a budget and try to stay within your means. CNET’s mortgage calculator below can help homebuyers prepare for monthly mortgage payments.

Home Buyers May Qualify For Low Downpayment Home Loan Options

Loan approval is subject to credit approval and program guidelines. Not all loan programs are available in all states for all loan amounts. Interest rates and program terms are subject to change without notice. Mortgage, home equity and credit products are offered by U.S. The interest rate is the amount of money your lender charges you for using their money.

Comparing common loan types

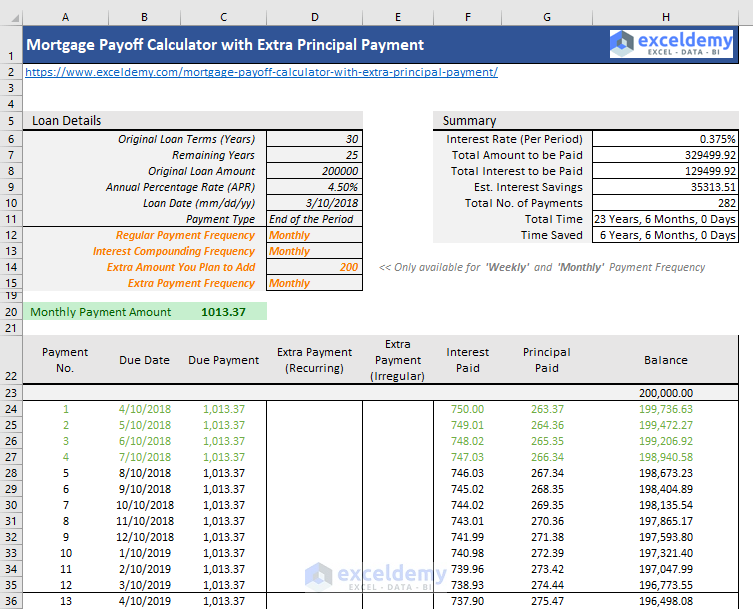

In general, residences situated in coastal areas and major cities have higher conforming limits. Using the above calculator can help you put together all of these complex variables to get a clear picture of your monthly mortgage payment so you know exactly how much to expect. The amortization chart shows the trend between interest paid and principal paid in comparison to the remaining loan balance. Based on the details provided in the amortization calculator above, over 30 years you’ll pay $351,086 in principal and interest. You can also adjust the interest rates to see your payments based on market conditions or your credit score.

Mortgage Calculator: PMI, Interest & Taxes - The Motley Fool

Mortgage Calculator: PMI, Interest & Taxes.

Posted: Thu, 09 Nov 2023 08:00:00 GMT [source]

Deciding how much house you can afford

Examples of other loans that aren't amortized include interest-only loans and balloon loans. The former includes an interest-only period of payment, and the latter has a large principal payment at loan maturity. When a borrower takes out a mortgage, car loan, or personal loan, they usually make monthly payments to the lender; these are some of the most common uses of amortization. A part of the payment covers the interest due on the loan, and the remainder of the payment goes toward reducing the principal amount owed. Interest is computed on the current amount owed and thus will become progressively smaller as the principal decreases.

With this article, we hope to help you choose the right mortgage for your prospective home. Unsecured loans generally feature higher interest rates, lower borrowing limits, and shorter repayment terms than secured loans. Lenders may sometimes require a co-signer (a person who agrees to pay a borrower's debt if they default) for unsecured loans if the lender deems the borrower as risky. The amount of cash a borrower pays upfront to buy a home; it goes toward the purchase price with mortgage loans typically used to finance the remaining amount. While it depends on your state, county and municipality, in general, property taxes are calculated as a percentage of your home’s value and billed to you once a year.

A down payment of 20% or more will get you the best interest rates and the most loan options. There are a variety of low-down-payment options available for home buyers. You may be able to buy a home with as little as 3% down, although there are some loan programs (such as VA loans and USDA loans) that require no money down. Long-term mortgages typically have higher rates but offer more protection against rising interest rates. Penalties for breaking a long-term mortgage can be higher for this type of term. If you’re hoping to buy a home, weeks or months could pass before you find a house and negotiate your way to an accepted offer.

Conforming conventional loans adhere to conforming limits set by the Federal Housing Finance Agency (FHFA). This is the prescribed cap on loan amounts you can borrow for conforming loans. Conforming limits may be lower or higher, depending on the location of the house.

A $2,000 per month mortgage payment is too much for borrowers earning under $92,400 a year, according to typical financial advice. A conservative or comfortable DTI ratio is usually considered to be anywhere from 1% to 26%, if you only include mortgage debt. A $2,000 per month mortgage payment represents a 26% DTI if you earn $92,400 per year. It calculates the remaining time to pay off, the difference in payoff time, and interest savings for different payoff options.

These penalties can amount to massive fees, especially during the early stages of a mortgage. With a fixed-rate loan, a larger portion of your payment goes toward the interest during the first several years of a loan. But towards the latter years of the loan, a greater part of your payments go toward the principal. As long as you keep making payments, your mortgage should be paid within 30 years.

As a rule, your combined household income (including all adults in the home) should not exceed more than 115% of the median family income in your area. You can check the prescribed income limits in your area by visiting this USDA map. However, the good news is there are other financing options out there that’s worth exploring.

Interest rates vary depending on the type of mortgage you choose. See the differences and how they can impact your monthly payment. Purchase price refers to the total amount you agree to pay to the property’s seller. This amount is typically different from your loan amount, since most lenders won’t loan you the full amount of a property’s purchase price.

No comments:

Post a Comment